The 8th Pay Commission salary hike is the single most consequential financial event for approximately 49 lakh serving central government employees and nearly 65 lakh pensioners in India. The Union Cabinet formally approved the constitution of the 8th Central Pay Commission on January 16, 2025, setting in motion a structured review of salaries, allowances, and pension structures — the first such revision since the 7th Pay Commission came into effect in January 2016.

Why the 8th Pay Commission Matters Beyond the Numbers

Every decade, India’s central pay commission exercise does more than adjust salary slips. It recalibrates the purchasing power of a large segment of the organised workforce, affects pension sustainability for retirees, and injects significant demand into the consumer economy. Government estimates suggest the combined fiscal impact of salary and pension revisions under the 8th CPC could inject between ₹3 lakh crore and ₹3.15 lakh crore into the economy.

For the employee sitting in a district-level office or a defence establishment, however, the conversation narrows to one number: how much will the take-home salary actually increase? That question does not yet have an official answer, but the structural evidence — from the commission’s Terms of Reference to DA trajectory and historical fitment patterns — allows for an informed analysis.

Current Status: Where Things Stand as of Early 2026

The commission has been formally approved but has not yet submitted its recommendations. The Terms of Reference were cleared by the Cabinet in November 2025. The commission comprises a Chairperson, one part-time member, and a Member-Secretary. It is expected to complete its work within 18 months of constitution, placing the final report submission around mid-2027.

This timeline creates a gap between the intended effective date of January 1, 2026 — which remains the reference date for pay revision — and the actual date when revised salaries will land in employees’ bank accounts. Based on precedent, the 7th Pay Commission was constituted in February 2014, submitted its report in November 2015, and the revised pay became effective from August 2016 (with January 2016 as the notional date). Employees received arrears to cover the interim period. The same pattern is expected to repeat under the 8th CPC.

Until the new structure is notified, central government employees continue receiving salary under the 7th Pay Commission framework, including bi-annual Dearness Allowance revisions. DA stood at 58% of basic pay from July 2025 and was expected to move to 60% from January 2026.

The Fitment Factor: The Number That Decides Everything

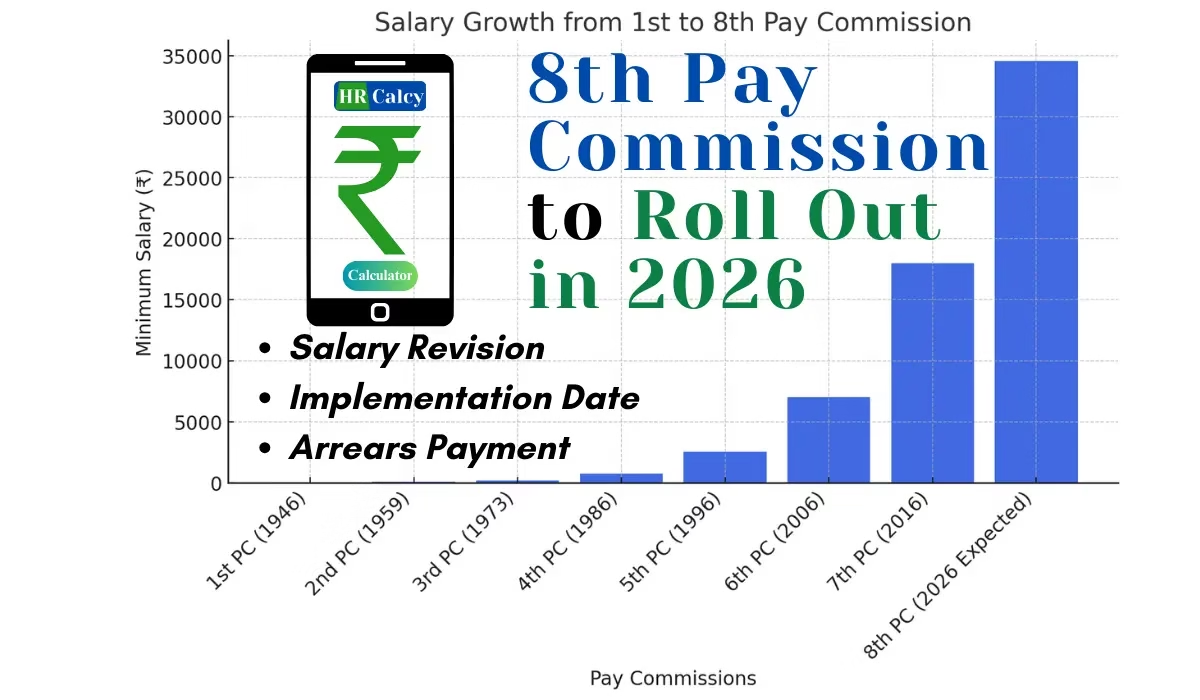

Under any Pay Commission, the fitment factor is the multiplier applied uniformly to the existing basic pay across all pay levels to arrive at the revised basic pay. The 7th Pay Commission used a fitment factor of 2.57, which raised the minimum basic pay from ₹7,000 (6th CPC) to ₹18,000. Understanding how that number was constructed helps decode what 8th CPC projections actually mean.

How the 7th CPC Fitment Factor Was Built

The 7th CPC first accounted for the inflation accumulated since the 6th CPC by merging the prevailing DA — which had reached 125% — into basic pay. This produced an inflation component of 2.25. On top of that, the commission added a real pay hike of approximately 14.22%, which brought the fitment factor to 2.57 (i.e., 2.25 × 1.1422). The headline figure of 2.57 masked the fact that the real income gain was only around 14%, with the bulk of the multiplier compensating for past inflation.

Applying the Same Logic to the 8th CPC

As of January 2026, DA under the 7th CPC is expected to be approximately 60%. Applying the same DA-merger methodology, the inflation component of the 8th CPC fitment factor would be 1.60 (i.e., 1 + 60% DA as a decimal). If the commission recommends the same 14.22% real pay hike as the 7th CPC, the resulting fitment factor would be approximately 1.83. That is the mathematical floor.

Employee unions and several expert groups are pushing for a higher real hike, given that the cost of living has increased substantially. Demands range from a fitment factor of 2.28 to as high as 3.00. The final number will depend on the commission’s assessment of fiscal capacity, inflation data, and the government’s acceptance of its recommendations.

| Fitment Factor Scenario | Current Basic Pay ₹18,000 | Current Basic Pay ₹35,400 | Current Basic Pay ₹56,100 |

|---|---|---|---|

| 1.83 (floor, 7th CPC method) | ₹32,940 | ₹64,782 | ₹1,02,663 |

| 2.28 (union demand, lower) | ₹41,040 | ₹80,712 | ₹1,27,908 |

| 2.57 (matches 7th CPC factor) | ₹46,260 | ₹90,978 | ₹1,44,177 |

| 2.86 (upper expert estimate) | ₹51,480 | ₹1,01,244 | ₹1,60,446 |

Note: Figures above represent revised basic pay only. HRA, TA, and other allowances are calculated separately on the new basic.

What the Nominal Salary Hike Actually Means: Nominal vs. Real

A common point of confusion — and occasional disappointment — around pay commission revisions is the gap between the headline percentage increase and the actual improvement in purchasing power.

At a fitment factor of 2.57 (matching the 7th CPC), an employee on a basic pay of ₹30,000 would see their basic revised to ₹77,100 — a 157% increase on paper. But if that employee was already receiving 60% DA (₹18,000), their effective pre-revision salary was ₹48,000. The jump to ₹77,100 represents a real increase of approximately 60.6%, not 157%. Once HRA and TA are recalculated on the new higher base, the gross take-home salary rises further, but the 157% headline must be read with appropriate context.

Real income gain at various fitment scenarios falls roughly in the 30% to 70% range, depending on accumulated DA, pay level, and city classification for HRA purposes.

Dearness Allowance and the Reset Mechanism

Every time a new Pay Commission is implemented, accumulated DA is absorbed into the revised basic pay and DA is reset to zero. Future DA hikes are then calculated on the new, higher basic — which means the same percentage DA translates to a larger absolute amount than before.

The Ministry of Finance has stated clearly that there is no proposal to merge DA with basic pay outside the pay commission framework. This matters because some reports had suggested a standalone DA merger. What will happen, consistent with past commissions, is that the DA prevailing at the time of 8th CPC implementation will be folded into the fitment factor calculation, and subsequent DA revisions will restart on the new base.

If DA reaches 60% by January 2026 and the commission’s fitment factor accounts for this, employees need not worry about “losing” their accumulated DA in the revision — it will be factored into the new basic.

Expected Salary Hike Percentages: A Realistic Range

Based on historical precedent and current projections, the overall salary hike under the 8th Pay Commission is expected to fall in the range of 20% to 34% in nominal terms over the pre-revision gross salary (including DA). The specific outcome depends on the fitment factor ultimately recommended and whether the government accepts it as proposed, modifies it, or rejects it in parts — all of which have happened in past commissions.

| Pay Commission | Fitment Factor Applied | Minimum Basic (Before) | Minimum Basic (After) | Avg. Overall Hike |

|---|---|---|---|---|

| 6th CPC (2006) | 1.86 | ₹2,750 | ₹7,000 | ~40% |

| 7th CPC (2016) | 2.57 | ₹7,000 | ₹18,000 | ~23–25% |

| 8th CPC (projected) | 1.83–2.86 | ₹18,000 | ₹33,000–₹51,480 | ~20–34% |

Revised Pay Matrix: What Will Change

The current 7th CPC pay matrix runs from Level 1 (minimum basic ₹18,000) through Level 18 (Cabinet Secretary equivalent, maximum ₹2,50,000). The 8th CPC will introduce a revised matrix where each level’s entry pay is the result of applying the new fitment factor to the corresponding 7th CPC entry pay.

For employees at the lower end — Groups C and D, which constitute the majority of the central government workforce — the relative percentage gain tends to be higher because the commission historically tilts towards compressing the ratio between minimum and maximum pay. Entry-level employees have consistently seen above-average percentage gains compared to senior officers in percentage terms, though absolute gains are obviously higher at the top.

The new pay matrix will also govern annual increment rates. Under the 7th CPC, a 3% annual increment was applied uniformly. Whether the 8th CPC introduces differentiated increment rates, links them to performance metrics, or retains the flat 3% structure is an active debate — employee unions strongly resist performance-linked increments, citing implementation challenges in large government departments.

Allowance Revisions: HRA, TA, and Others

Basic pay revision triggers a cascade of changes across the entire compensation package. The House Rent Allowance, currently set at 27%, 18%, and 9% of basic pay for X, Y, and Z category cities respectively, will be recalculated on the revised basic. HRA percentages themselves may also be revised upward if the commission finds them misaligned with actual rental market conditions in major cities.

Transport Allowance, which is tier-based rather than a straight percentage of basic, will also be revised. Medical facilities, children’s education allowance, and other statutory benefits are typically reviewed and adjusted in parallel with the main pay revision. Together, these secondary revisions contribute meaningfully to the overall improvement in take-home pay beyond what the fitment factor alone implies.

Impact on Pensioners: Minimum Pension and Parity

The 8th Pay Commission is expected to be as significant for the approximately 65 lakh central government pensioners as it is for serving employees. The minimum pension under the 7th CPC stands at ₹9,000 per month. Applying the projected fitment factors, the revised minimum pension could range from ₹16,470 (at 1.83) to ₹25,740 (at 2.86).

The issue of pension parity — ensuring that pensioners who retired at different points in time receive comparable pensions — has been a recurring demand. The 7th CPC introduced the Option-1 method to address this, though implementation remained contested. The 8th CPC is expected to revisit the parity formula with a cleaner methodology.

Pensioners who retired before January 1, 2026 remain eligible for revision under the 8th CPC once recommendations are notified, provided the government confirms this. The Finance Ministry has not restricted the revision to employees serving after the cut-off date, consistent with all previous commissions.

Arrears: When Will Employees Receive Backdated Pay

Since the 8th CPC’s reference date is January 1, 2026, but the actual salary revision will take effect months or years later, employees will accumulate arrears for the intervening period. The 7th CPC took approximately eight months from the reference date to actual implementation, and arrears were paid in a lump sum.

If the 8th CPC follows a similar timeline — which is optimistic given that the commission itself has 18 months to submit its report — arrears could accumulate for 12 to 24 months or more. At higher pay levels with larger monthly differentials, this could represent a substantial one-time payment. However, arrears attract full income tax in the year of receipt, unless employees opt for relief under Section 89(1) of the Income Tax Act and file Form 10E.

Salary Calculation: How to Estimate Your Revised Pay

While the official pay matrix is pending, the underlying formula for basic pay revision is well-established. The revised basic pay is calculated by multiplying the current 7th CPC basic pay by the fitment factor. Gross salary is then built up by adding DA (calculated as a percentage of the new basic), HRA (based on city category), and applicable transport and other allowances.

The formula in simplified form:

Revised Basic Pay = Current Basic Pay × Fitment Factor

Gross Salary = Revised Basic Pay + DA + HRA + TA + Other Allowances

To run a detailed estimate accounting for your specific pay level, city category, HRA tier, transport allowance eligibility, NPS deduction, and applicable income tax, the 8th Pay Commission Salary Calculator on HR Calcy allows you to input actual parameters from your pay slip and model different fitment factor scenarios side by side.

For a broader understanding of how pay levels map to pay bands and grade pays across all levels, the detailed 8th CPC pay revision guide on HR Calcy covers the 7th CPC base matrix that will serve as the starting point for all 8th CPC calculations.

The Questionnaire Process and Employee Input

The 8th Pay Commission launched an online questionnaire on the MyGov portal inviting suggestions from serving employees, pensioners, and other stakeholders. The deadline for submissions was set for March 16, 2026. Inputs gathered through this process will inform the commission’s deliberations on salary structure, fitment factor, allowance revision, and pension methodology.

This consultation is standard practice — prior commissions also solicited employee and pensioner federation inputs. While individual submissions carry less weight than federation-level representations, the aggregate data on employee expectations, cost-of-living concerns, and regional disparities does feed into the commission’s working papers.

State Government Employees: A Separate Timeline

The 8th Pay Commission’s scope is limited to central government employees, defence personnel, and central government pensioners. State government employees are governed by separate state pay commissions, which typically follow the central commission’s lead with a lag of one to three years. Several states historically adopt the central fitment factor but adjust for their own fiscal conditions, often extending implementation timelines or modifying the structure of allowances.

For state employees, the 8th CPC still matters because it sets the benchmark that state commissions will reference. Employees in states that closely mirror central pay structures — including many major states — should watch the 8th CPC recommendations carefully as early signals of what their own pay revision may deliver.

Economic and Fiscal Implications

The central government’s wage and pension bill runs at a significant proportion of total revenue expenditure. The 7th CPC implementation in 2016 increased the pay and pension bill by approximately ₹1.02 lakh crore in the first year. The 8th CPC is expected to have a larger absolute impact, with current estimates placing the additional annual fiscal burden between ₹1.5 lakh crore and ₹1.8 lakh crore.

This fiscal outflow is not uniformly negative from an economic standpoint. Government employees with stable incomes tend to direct consumption towards housing, consumer durables, and financial products — sectors that benefit meaningfully from salary revision cycles. The Reserve Bank of India and independent economists have historically noted a mild inflationary impulse from pay commission implementations, particularly in non-tradable services, but the demand stimulus effect is generally viewed as net positive at the macroeconomic level.

Key Uncertainties and What to Watch

Several variables remain unresolved as of early 2026. The fitment factor is the most consequential unknown, and the gap between union demands (2.28 to 3.00) and the methodological floor (1.83) is wide enough that the commission’s recommendation could produce very different outcomes depending on where it lands.

The treatment of DA at the time of implementation — specifically whether accumulated DA will be fully absorbed into the fitment factor or handled differently — is a secondary but important variable. The Finance Ministry has consistently resisted standalone DA mergers, which provides some confidence that the commission will handle this through the standard fitment methodology.

Performance-linked pay elements, if introduced, could create differentiation within pay levels that the current uniform increment structure does not produce. Whether the government is willing to accept the administrative and political complexity of such a change remains an open question.

Finally, the timeline itself is subject to delay. Pay commissions historically take longer than their mandated submission deadline. Employees should plan their financial decisions on the basis that revised salaries are unlikely before late 2027, with January 2026 arrears being the probable mechanism for bridging the gap.

Practical Guidance for Employees and Pensioners

For employees approaching retirement in 2026 or 2027, the timing decision relative to the 8th CPC implementation carries real financial consequences. Retiring before the revised pay is notified means pension is fixed at 7th CPC levels, with 8th CPC revision applied subsequently. Retiring after implementation locks in the higher basic as the pension base from day one. Consulting a financial planner who understands government service conditions is worth the effort if retirement is within two to three years.

For serving employees, the most productive action now is accurate self-assessment. Know your current pay level and basic pay precisely. Identify your city category for HRA, and verify your transport allowance eligibility. When the commission’s recommendations are eventually notified, having this baseline clear will allow you to verify the pay fixation statement issued by your accounts office against the official pay matrix — discrepancies in fixation are not uncommon, and the window to raise objections is typically limited.

For pensioners, maintain records of your last drawn basic pay, retirement date, and PPO number. The pension revision process under previous commissions has involved a structured form submission to the pension disbursing authority, and having documentation ready reduces processing delays.

FAQ

What is the expected fitment factor under the 8th Pay Commission?

The fitment factor under the 8th Pay Commission has not been officially confirmed. Based on the 7th CPC methodology — which absorbed accumulated DA and added a real pay hike — experts project the fitment factor to fall between 1.83 and 2.86, with employee unions demanding a minimum of 2.28 to 3.00.

From which date will the 8th Pay Commission salary hike be effective?

The reference date for the 8th Pay Commission salary revision is January 1, 2026. Actual disbursement will occur after the commission submits its report and the government accepts the recommendations, with arrears paid from January 1, 2026 to cover the interim period.

What will be the minimum basic pay after the 8th Pay Commission revision?

The current minimum basic pay of ₹18,000 under the 7th CPC will be revised by applying the 8th CPC fitment factor. At the projected floor of 1.83, the revised minimum basic pay would be approximately ₹32,940, rising to ₹51,480 if a fitment factor of 2.86 is applied.

Will Dearness Allowance be merged with basic pay under the 8th Pay Commission?

The Ministry of Finance has confirmed there is no standalone proposal to merge DA with basic pay. However, as with all previous pay commissions, the DA accumulated up to the implementation date will be factored into the fitment factor calculation, effectively absorbing it into the revised basic pay structure.

Are state government employees covered under the 8th Pay Commission?

No. The 8th Pay Commission’s mandate covers only central government employees, defence personnel, and central government pensioners. State government employees are governed by separate state pay commissions, which typically follow the central commission’s recommendations with a lag of one to three years.